Cryptocurrency is no longer confined to the fringe of organised crime and tech companies. The age of ‘digital currency’ has well and truly arrived and many Australians have taken to investing in crypto. Tax myths abound and not surprisingly, regulators worldwide, including the ATO, are on the case.

This progression is not surprising given the extensive media coverage of the extraordinary volatility of cryptocurrency over the last 12 months. And what a ride it has been, with returns of up to 1,000% during the bull run in the first half of this year followed by the equally dramatic bear market last month brought about events including Tesla’s u-turn on accepting Bitcoin as payment and the Communist Party of China’s decree to ban the use of cryptocurrency in China, the world’s second largest economy and the location of 90% of the world’s cryptocurrency mining operations.

Cryptocurrency is a relatively new concept for most and has many complicated aspects that are difficult to grasp unless you are tech savvy. This has led to a lot of misinformation generated about this class of asset. Cryptocurrency has been written about previously in this Bulletin and no doubt more will be written as time progresses. This article aims to clear up some of the misinformation about the tax treatment of cryptocurrency.

So let’s address some of the common myths about the taxation of cryptocurrency circulating and the facts countering these myths.

Myth: Cryptocurrency is a currency for taxation purposes

No, it is not a currency for taxation purposes.

Seems counter intuitive given we refer to “cryptocurrency”, however the ATO does not regard bitcoin (and other cryptocurrencies) as a ‘currency’ (nor ‘foreign currency’) for the purpose of applying Australian tax law.

The term ‘Currency’ is not defined in the Income Tax Assessments Acts, however, takes its meaning under Australian law by virtue of the Currency Act 1965 (the Currency Act). In summary, the Currency Act provides that the essential characteristic of currency is State recognition and adoption of a monetary unit under law.

Under the Currency Act, the unit of currency of Australia is the Australian Dollar and is the only recognised form of payment besides the currency of some other country.

The wisdom has been that as no cryptocurrency has been adopted as a monetary unit recognised and adopted by the laws of any other sovereign State, it is not ‘foreign currency’.

However, we await the regulatory response to El Salvador officially adopting Bitcoin as legal tender from 7 September 2021!

Will Bitcoin be the first cryptocurrency to succeed as a “proper” currency?

Why is this important?

Gains or losses on cryptocurrency are not dealt with in the same way as foreign currency transactions.

Cryptocurrency is a dealt with as a CGT asset as outlined below.

Reality: Cryptocurrency is a CGT asset for taxation purposes

If cryptocurrency is not a ‘currency’ for taxation purposes, then what is it?

Cryptocurrency is a ‘CGT asset’ for taxation purposes. Generally, the tax consequences of a disposal of cryptocurrency are dealt with under the CGT provisions. Under the CGT provisions, a taxpayer will make a capital gain from the disposal of cryptocurrency if the capital proceeds from the disposal of the cryptocurrency are more than the cryptocurrency’s cost base. Conversely, a capital loss will result if the capital proceeds are less than the cost base.

The capital proceeds from the disposal of the cryptocurrency consist of:

- The money or the market value of any other property received (or entitled to be received) by the taxpayer in respect of the disposal.

The cost base of the cryptocurrency will consist of:

- The money paid or the market value of any other property the taxpayer gave in respect of acquiring the cryptocurrency.

Where the taxpayer has held the cryptocurrency for less than 12 months, the whole capital gain will be included in assessable income. Where the taxpayer has held the cryptocurrency for at least 12 months, any capital gain may be reduced by a 50% discount and only half the gain is included in the taxpayer’s assessable income.

We note the general discount is 33% for complying superannuation funds and does not apply to corporate taxpayers.

Ordinary income

There are 2 main circumstances where the gains on the disposal of cryptocurrency will be assessed as ordinary income rather than a capital gain. This would occur where the taxpayer is considered to have acquired the cryptocurrency:

- In the course of carrying on a business; or

- As part of a profit-making undertaking.

When assessed as ordinary income, there is no 50% general discount on the gain irrespective of how long the cryptocurrency has been held prior to disposal. Whether such gains give rise to ordinary income or CGT consequences will depend on the particular facts and circumstances of the taxpayer. It can become a complex task to determine whether a transaction should be on capital or revenue account.

Generally, the more ‘business like’ approach taken by the taxpayer in respect of cryptocurrency, the more likely gains on the disposal of cryptocurrency will be assessed as ordinary income. The obvious distinction would be between a taxpayer that acquires cryptocurrency to hold long term with infrequent trades versus a taxpayer that day trades cryptocurrency to make gains on short-term volatility. The former taxpayer is more likely to have gains assessed under the CGT provisions while the later as ordinary income.

There are a number of conditions that are considered when determining whether a taxpayer is carrying on a business and none of them is determinative in insolation. These factors include the size, scale and sophistication of the operation, the frequency of transactions, the level of organisation, record keeping required and a profit-making intention. Below are some examples where a taxpayer’s gains are more likely to be assessed as ordinary income rather than as a capital gain:

- The taxpayer is carrying on a business of mining and selling cryptocurrency.

- The taxpayer carries on a cryptocurrency exchange business.

- The taxpayer carries on a business where cryptocurrency is held for the purposes of sale or exchange in the ordinary course of the business.

- The taxpayer carries on high volume trading of cryptocurrency with the intention to make gains from short term fluctuations in the cryptocurrency volatility.

Myth: My gains from cryptocurrency are tax-free if my cost of investment in cryptocurrency is less than $10,000

There is a misconception that gains from cryptocurrency are tax-free if the cost of acquiring the holding is less than $10,000.

This is not correct, although gains on cryptocurrency qualifying as a personal use asset are tax-free where the cost of investment is less than $10,000.

A personal use asset is a CGT asset, other than a collectable, that is used or kept mainly for the personal use or enjoyment of the taxpayer.

A capital gain from a personal use asset is CGT exempt if it is acquired for $10,000 or less. Any capital losses from the disposal of personal use assets are disregarded.

Unfortunately, there is very little guidance from the ATO on its views about the definition of ‘personal use assets’.

Cryptocurrency may be a personal use asset if it is acquired and kept mainly to purchase items for personal use or consumption.

There are private rulings that indicate the ATO will regard bitcoin acquired in the early stages of its evolution as a personal use asset where it is demonstrated the taxpayer acquired the bitcoin out of personal technological interest rather than a profit-making intention. In these circumstances, the acquisition of bitcoin was accepted to be more in the nature of a hobby and therefore treated as a ‘personal use asset’.

Given rapid development of the digital currency market in recent years and the increase in value invested in cryptocurrency, I expect it would be far more difficult to convince the Commissioner that holdings of cryptocurrency were acquired in the course of a hobby.

Reality: Cryptocurrency may be regarded as a personal use asset in only very limited circumstances

As noted above, cryptocurrency may be a personal use asset in limited circumstances.

The most common scenario where cryptocurrency would be treated as a personal use asset would be where taxpayer acquires cryptocurrency to facilitate a purchase of personal services or assets in the short term. For example, John acquires bitcoin through an exchange to facilitate payment to purchase a couch for his home from a supplier which accepts bitcoin as payment for its products.

To further illustrate the limited circumstances where cryptocurrency would be regarded as a personal use asset, we outline below a private ruling issued by the Commissioner which found a taxpayer could treat some of their bitcoins as personal use assets but not others. The distinction was determined by reference to the taxpayer’s circumstances at the time of acquiring the bitcoin.

In the private ruling discussed above, the taxpayer stated to the Commissioner that he:

- had a long-standing interest in computers, in the course of which he became interested in Bitcoin during its very early stages. The taxpayer was also drawn to Bitcoin as a solution to money issuance in light of the events of the global financial crisis and sub-prime mortgage crisis in the United States;

- began to acquire and mine bitcoin, and did so with a view to exploring and learning about the technology and participating in the community associated with Bitcoin. The taxpayer did not have a view to profit from any future increase in the value of the bitcoins;

- had not engaged in any business related to bitcoins;

- still held the majority of bitcoin he ever owned.

The bitcoin held by the taxpayer was divided into 4 categories based on the circumstances at the time of acquisition as follows:

- Bitcoins purchased informally: During the very early stages of Bitcoin’s existence, the taxpayer purchased bitcoins informally via an Internet discussion board.

- Bitcoins mined personally: During the very early stages of Bitcoin’s existence, the taxpayer ran the bitcoin mining software on his personal computer, yielding bitcoins.

- Bitcoins mined as part of a pool: The taxpayer mined bitcoin as part of a ‘pool’, where any bitcoins obtained by pool members were split with the others.

- Bitcoins purchased through an online exchange: At a later stage where Bitcoin had matured somewhat as a financial instrument, the taxpayer purchased a number of bitcoins by depositing Australian dollars to the exchange’s bank account.

Circumstance 1 and 2: Bitcoins purchased informally and bitcoins mined personally

ATO decision

Bitcoin acquired in circumstances 1 and 2 above was a personal use asset.

Reasoning

The taxpayer acquired the bitcoin in its early stages for the sake of having it, to tinker with, to experience the process and/or to participate in the community, possibly with an incidental thought that the thing might be worth something one day as opposed to a specific intention to profit or use the bitcoin as a long-term store of value.

Circumstance 3: Bitcoins mined as part of a pool

ATO decision

Bitcoin acquired in circumstance 3 was not a personal use asset.

Reasoning

At the time of acquiring the bitcoins, the Bitcoin network had matured, as evidenced by the higher difficulty which led to the need to use a pool. A pool involves cooperation in order to obtain something of value, which puts the activity closer to the commercial end of the spectrum rather than the personal.

Circumstance 4: Bitcoins purchased through an online exchange

ATO decision

Bitcoin acquired in circumstance 4 was not a personal use asset.

Reasoning

In light of the taxpayer’s personal financial circumstances, financial capacity and the amount spent by the taxpayer to acquire the bitcoin, the Commissioner determined the ‘category 4’ bitcoin was most likely acquired with the intent to seek an exchange gain or at least storing value, as opposed to personal use or enjoyment. Accordingly, it was less likely to characterise this acquisition as part of a hobby or for the purpose of covering immediate personal living expenses.

It should be noted that private binding rulings only protect the specific taxpayer and are applied to their specific circumstances. The issued private binding ruling cannot be relied upon by other taxpayers to apply to their own circumstances. Any taxpayer who believes their cryptocurrency should be regarded as a personal use asset should seek professional tax advice and consider seeking their own private ruling.

Myth: Exchanging one cryptocurrency for another is not subject to tax

There is a common misconception that tax is only calculated when I “cash in” my cryptocurrency back to Australian dollars.

Other than the limited circumstances where cryptocurrency is held as a personal use asset, any gain on the exchange of one cryptocurrency for another will be liable to tax as either a capital gain or ordinary income depending on the taxpayer’s circumstances.

It should be noted that transferring cryptocurrency from one wallet to another wallet is not considered the disposal of cryptocurrency for tax purposes as the taxpayer maintains ownership of the coin/token.

Tip: Taxpayers need to be wary they do not end up with an unfunded tax liability arising from the exchange of one cryptocurrency for another.

For example, John makes a substantial taxable capital gain on the exchange of Bitcoin for Ethereum in the 2021 tax year. John is required to pay tax on this gain by 15 May 2022. John waits until the May 2022 deadline to pay his 2021 tax liability but does not have sufficient cash and has to cash in some of his Ethereum to satisfy the debt. John is exposed to a fall in the price of Ethereum and may be forced to cash in his Ethereum during a bear market. John could even end up in a situation where his entire Ethereum holding is not sufficient to cover his tax liability.

When exchanging cryptocurrency for cryptocurrency, we recommend taxpayers assess their tax liability and consider if they should cash in some of their gain early to cover their future tax liability so they are not forced to sell down in a potential bear market.

Myth: Cryptocurrency is anonymous so tax authorities won’t know if I buy or sell cryptocurrency

Due to the perceived higher level of anonymity in the digital world than the physical world, some taxpayers falsely believe the ATO will never know if they hold cryptocurrency.

Detection risk may have been lower during the early stages of cryptocurrency but the ATO now has systems in place to monitor the digital currency markets. ATO data analysis shows a dramatic increase in trading since the beginning of 2020. It is estimated that there are over 600,000 taxpayers that have invested in crypto-assets in recent years.

The ATO announced in May 2021 that it will be writing to around 100,000 taxpayers with cryptocurrency assets explaining their tax obligations and urging them to review their previously lodged returns.

The ATO also announced that it expects to prompt almost 300,000 taxpayers as they lodge their 2021 tax returns to report their cryptocurrency capital gains or losses.

On 28 May 2021, the ATO issued a Media Release titled “Cryptocurrency under the microscope this tax time”. In this media release, Assistant Commissioner Tim Loh said:

“While it appears that cryptocurrency operates in an anonymous digital world, we closely track where it interacts with the real world through data from banks, financial institutions, and cryptocurrency online exchanges to follow the money back to the taxpayer.”

The ATO matches data from cryptocurrency designated service providers to individuals’ tax returns in order to ensure investors are paying the right amount of tax.

Important: Taxpayers must remember there are significant penalties for under-declaring income.

Reality: The ATO is increasing efforts to monitor digital currency markets and continues to share information with foreign tax authorities

On 9 June 2021, the ATO gave notice of its data matching program in respect of cryptocurrency for the 2020-21 to 2022-23 financial years.

The ATO will acquire account identification and transaction data from cryptocurrency designated service providers for 2020-21 to 2022-23 inclusively. The data items include:

- taxpayer identification details (names, addresses, date of birth, phone numbers, social media account and email addresses), and

- transaction details (bank account details, wallet addresses, transaction dates, transaction time, transaction type, deposits, withdrawals, transaction quantities and coin type).

The ATO estimates that records relating to approximately 400,000 to 600,000 individuals will be obtained each financial year. The data will be acquired and matched to ATO systems to identify and treat taxpayers who failed to report a disposal of cryptocurrency in their income tax return.

The reach of the ATO to monitor digital currency markets extends well beyond our shores. In 2018, the ATO joined tax enforcement authorities from Canada, the Netherlands, the United Kingdom and the United States to establish the joint operational alliance known as the J5 to increase collaboration in the fight against international and transnational tax crime and money laundering. The J5 is focused on cross-national tax crime threats including cyber-crime and cryptocurrency as well as enablers of global tax evasion, while working to share intelligence and data in near real time.

Tips for taxpayers holding cryptocurrency

Maintain accurate records

Taxpayers need to keep records of all their transactions associated with acquiring, holding and disposing of cryptocurrency. They will need to keep records for 5 years after they dispose of cryptocurrency.

When acquiring cryptocurrency, remember to keep receipts of transactions, or documents that display:

- The cryptocurrency.

- The purchase price in AUD.

- The date and time of the transaction.

- What the transaction was for.

- Commission or brokerage fees on the purchase.

- Agent, accountant and legal costs.

- Exchange record.

While holding cryptocurrency, taxpayers should remember to keep:

- Software costs related to managing their tax affairs.

- Digital wallet records and keys.

- Documents showing the date and quantity of cryptocurrency received via staking or airdrop.

When disposing of cryptocurrency, remember to keep receipts of sale or transfer, or documents that display:

- The cryptocurrency.

- The sale or transfer price in AUD.

- The date and time of the transaction.

- What the transaction was for.

- Commission or brokerage fees on the sale or transfer.

- Exchange records.

- Calculation of capital gain or loss.

There are many platforms and software packages available to assist taxpayers keep track of movements in their cryptocurrency.

Understand how crypto transactions will be treated for tax purposes

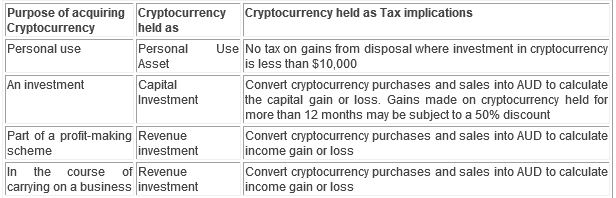

To sum up, taxpayers will need to assess whether they hold their cryptocurrency as outlined in the table below.

This article was first published in Thomson Reuters’ Weekly Tax Bulletin.